Table of Contents

Introduction: What is PM Street Vendor’s AtmaNirbhar Nidhi (PM SVANidhi) scheme?

PM Street Vendors AtmaNirbhar Nidhi (PM SVANidhi) is a micro-credit scheme launched by the Central Government to provide working capital in terms of loans to Street Vendors so that they can tied over the Covid-19 situation.

The scheme was launched on June 2020 by the Ministry of Housing and Urban Affairs. This scheme is meant to improve the livelihoods of street vendors.

The scheme has been extended till March 2022.

Who is a Street Vendor under PM SVANidhi?

Street Vendor/ Hawker/ Thelewala are classified as one if they provide goods and services at doorstep of people in cities. These goods include vegetables, fruits, ready-to-eat food, tea, pakodas, bread, textile, footwear, artisan products, stationery, etc. Services also include Barber Shops, pan shops, laundry services, etc.

Objectives of the PM SVANidhi scheme?

- To provide working capital loan upto 10,000

- Incentivize regular repayment like giving interest subsidy @7% per annum will be credited directly to bank account every quarter

- Reward digital transactions

- No penalty on early repayment of the loan

Benefits of the PM SVANidhi scheme?

- Urban Street vendors are eligible for 10,000 working capital loan with no collateral

- 1 year easy repayment options given by financial institutions

- No penalty charged for repayment before scheduled date

- To promote digial payment, cash bank in range to 50 to 100 Rupees based on the number of digital transactions

Eligibility Criteria for PM SVANidhi scheme

- Street Vendors in possession of the certificate of Vending / identity card issued by Urban Local Bodies (ULB) or possession certificate if the Vending/identity card if not yet issued

- Letter of Recommendation (LOR) issued by Urban Local Bodies/ Town Vending Committee (TVC) if they are not part or have been left out of the ULB survey. The following documents are required if they have been left out of the ULB survey

- Documents from a previous loan from a NBFC or bankor MFI with the intention of vending or

- Information about membership details, if you are a you are a member of a street vendor’s associations such as NASVI, NHF, SEWA etc. or

- Other documents that prove that the person is a vendor;

- The vendor may also request ULB via a straightforward application on white paper. It will then conduct a local inquiries to determine the authenticity of their claim for receiving LoR.

- KYC documents : Aadhaar card/ Driving Licence/ Voter identity card/ PAN card/ MNREGA card

Is the Street Vendors who have left the cities during Covid-19 eligible for PM SVANidhi scheme?

In case, the beneficiaries have left the cities and have gone back to their villages or home towns they are eligible for loans under the PM SVANidhi scheme once they return to cities. They can avail loan under the scheme and restart their work.

How to apply online for PM SVANidhi scheme?

You can visit PM SVANidhi website and apply for the scheme online by using your mobile no

Where to find PM SVANidhi scheme guidelines?

You can find the entire scheme details on the PM SVANidhi website. Please click here

If you want to download the entire scheme details, you can also download by clicking here

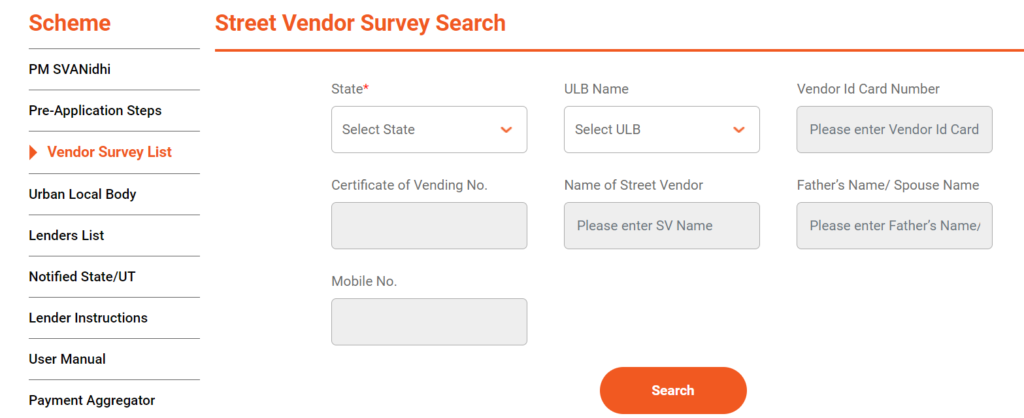

How to find if your name is on the Street Vendor list?

Visit the PM SVANidhi website and click on “Scheme Instructions” and then click on “Vendor Survey List”. I have given a direct link to the website

Fill in the details and click on search.

Which Financial instructions provide loan under this scheme?

Scheduled Commercial Banks, Regional Rural Banks (RRBs), Small Finance Banks (SFBs), Cooperative Banks, Non-Banking Finance Companies (NBFCs), Micro Finance Institutions (MFIs) & SHG Banks established in some States/UTs.

Who provides Credit Guarantee for the loans?

The scheme provides a guaranteed cover to financial institutions if they suffer a loss and it is provided in a graded manner. It is provided a basis on the below category of the loss

- First Loss Default (Up to 5%): 100%

- Second Loss (beyond 5% up to 15%): 75% of default portfolio

- Max. guarantee coverage will be 15% of the year portfolio.

Implementation Partner for the scheme

Small Industries Development Bank of India (SIDBI) will be the implementation partner of the Ministry of Housing and Urban Affairs for scheme administration. SIDBI will work with other identified financial institutions.

You may also be interested in Pradhan Mantri Suraksha Bima Yojana(PMSBY), click here.